Texas Homeowners Insurance Rates Have Surged: What Central Texas Homebuyers Need to Know

By James Walker, Associated Broker | Team Lead, Walker Texas Team | Keller Williams Realty

If you’re thinking about buying a home in Texas, Texas homeowners insurance rates need to be part of the conversation before you decide what you can afford.

Over the last five years, homeowners insurance has become a much larger part of the cost of owning a home. In fact, recent reporting based on Texas Department of Insurance data found that the average Texas homeowners policy cost about $3,500 in 2025, compared with roughly $2,000 in 2020—an increase of approximately 80%. (Texas Department of Insurance)

As an Associated Broker and Team Lead of the Walker Texas Team at Keller Williams Realty, I work with buyers and sellers throughout Central Texas. Increasingly, one of the biggest surprises buyers face isn’t always the mortgage rate or property taxes. It’s the cost of insuring the home.

The good news is that the pace of statewide rate increases slowed sharply in 2025. However, that doesn’t mean insurance has suddenly become inexpensive.

Let’s take a closer look at what has happened and, more importantly, what it means if you’re buying a home in Central Texas.

Aerial view of 97 W Mimosa Circle in the highly desirable Spring Lake Hills neighborhood of San Marcos, Texas.

Texas Homeowners Insurance Rates Changed Dramatically

The most useful way to understand the last several years is to look at the average annual rate changes rather than assume every homeowner paid the same premium.

Texas Department of Insurance data reported for recent years shows just how quickly the market changed.

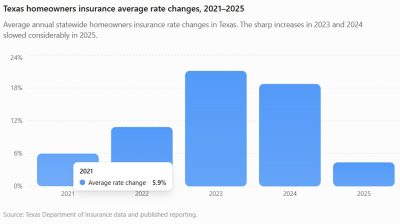

Texas Homeowners Insurance Average Rate Changes

| Year | Average Rate Change |

|---|---|

| 2021 | 5.9% |

| 2022 | 10.8% |

| 2023 | 21.1% |

| 2024 | 18.7% |

| 2025 | 4.3% |

Texas homeowners insurance rates rose most sharply in 2023 and 2024 before the average statewide rate increase slowed considerably in 2025. Source: Texas Department of Insurance data and published reporting.

The graph tells an important story.

Rates were already rising in 2021 and 2022. Then, the increases accelerated dramatically in 2023 and 2024. In 2025, however, the average statewide rate increase slowed to 4.3%.

That slowdown is encouraging. Nevertheless, homeowners are still paying premiums built on top of several years of previous increases.

In other words, a smaller increase is not the same thing as a decrease.

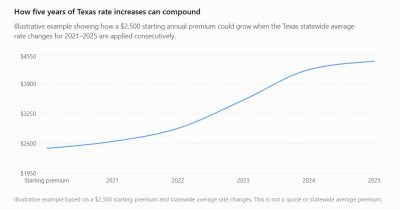

What Five Years of Insurance Increases Can Look Like

Insurance premiums vary too much from one house to another to claim that every $400,000 Texas home followed the same path.

Location matters. So do the home’s age, roof, construction, coverage limits, deductibles, claims history, insurer, and many other underwriting factors.

However, we can use a hypothetical example to show how compounding rate increases work.

Suppose a Texas homeowner began with a $2,500 annual premium. Applying the statewide average rate changes shown above would produce approximately the following result:

| Period | Illustrative Annual Premium |

|---|---|

| Starting premium | $2,500 |

| After 2021 increase | $2,648 |

| After 2022 increase | $2,933 |

| After 2023 increase | $3,552 |

| After 2024 increase | $4,216 |

| After 2025 increase | $4,397 |

That is an increase of approximately 76% from the starting premium.

An illustrative example shows how a $2,500 starting annual premium could grow to approximately $4,397 after applying Texas statewide average rate changes from 2021 through 2025.

This example helps explain why homeowners may feel that insurance costs have exploded, even though the 2025 increase was much smaller than the increases in 2023 and 2024.

It also shows why buyers should never estimate future insurance costs based on what a friend, neighbor, or previous homeowner pays.

Why Have Texas Homeowners Insurance Rates Increased?

There isn’t one single reason. Instead, several pressures have hit the Texas insurance market at the same time.

Severe Weather and Catastrophic Losses

Texas faces an unusually broad range of weather risks.

Depending on where you live, those risks can include:

- Hail

- High winds

- Tornadoes

- Hurricanes

- Flooding

- Wildfires

- Hard freezes

- Severe thunderstorms

Texas has experienced dozens of billion-dollar disasters in recent years. Every major event can generate thousands of insurance claims and billions of dollars in losses.

Central Texas may be far from the Gulf Coast, but we aren’t immune. Hail, wind, wildfire risk, hard freezes, and severe storms can all affect insurance pricing.

Severe thunderstorms, lightning, hail, high winds, and other weather events are among the risks that can contribute to homeowners insurance claims and rising costs in Texas.

The Cost to Repair or Rebuild a Home Has Increased

A home’s market value and its insurance replacement cost are not necessarily the same thing.

That’s an important distinction.

Homeowners insurance is heavily influenced by what it could cost to repair or rebuild the structure after a covered loss. Therefore, increases in labor, roofing, lumber, HVAC equipment, and other construction materials can affect premiums.

Even if the resale value of a home falls, the cost to rebuild it may remain high.

That is one reason a softer real estate market does not automatically mean cheaper homeowners’ insurance.

Read about other costs of buying a home here:

Mortgage Rates in Central Texas Rise Again: – Walker Texas Team

How Inflation Affects Homeownership – Walker Texas Team

Why Two Similar Central Texas Homes Can Have Very Different Insurance Costs

This is something I believe every buyer should understand.

Two homes with similar sale prices—even two homes in the same general area—can receive very different insurance quotes.

Factors may include:

- Roof age and condition

- Construction type

- Property location

- Prior claims

- Replacement cost

- Deductible choices

- Coverage limits

- Wildfire, wind, hail, or flood exposure

- Insurance carrier

- Individual underwriting factors

For example, an older home with an aging roof may cost substantially more to insure than a newer home at a similar purchase price.

Therefore, buyers shouldn’t wait until the last minute to investigate insurance.

What Does This Mean for a $400,000 Central Texas Home?

Let’s say you’re considering purchasing a $400,000 home.

The purchase price alone does not tell you what the insurance premium will be.

One buyer might receive a relatively competitive quote. Another buyer looking at a different $400,000 property could receive a much higher quote because of the roof, location, replacement cost, or other risk factors.

That’s why I don’t recommend using one statewide “average premium” as your personal budget.

Instead, get an actual quote for the specific property you’re considering.

A difference of $2,400 per year in insurance equals $200 per month. That can materially change the affordability of a home.

Homebuyers Should Look Beyond the Mortgage Payment

For years, many buyers focused primarily on the principal and interest portion of their mortgage.

Today, that’s not enough.

The true monthly cost of owning a home may include:

- Principal and interest

- Property taxes

- Homeowners insurance

- HOA dues

- Flood insurance, when applicable

- Maintenance and utilities

As a result, two homes with the same purchase price can have very different monthly ownership costs.

Start your home search here: Category Archives – Walker Texas Team

Get an Insurance Quote Early in the Home-Buying Process

When I work with buyers in San Marcos, New Braunfels, Kyle, Buda, Wimberley, Canyon Lake, Seguin, Martindale, and surrounding Central Texas communities, I recommend investigating insurance costs early.

Ideally, buyers should:

- Ask about the age and condition of the roof.

- Obtain an insurance quote for the specific property.

- Review the deductible—not just the annual premium.

- Ask what is and isn’t covered.

- Determine whether separate flood insurance should be considered.

- Compare the total monthly housing cost before making a final decision.

An inexpensive premium isn’t necessarily a good deal if the deductible or coverage leaves you exposed.

Likewise, the lowest-priced house isn’t always the least expensive house to own.

Explore Homes for Sale in San Marcos TX | Walker Texas Team

Moving to San Marcos TX | Local Guide – Walker Texas Team

Don’t Forget About Flood Insurance

Another important point is that a standard homeowners insurance policy generally does not cover flood damage.

Flood insurance is a separate consideration.

This matters in Texas, including areas well beyond the Gulf Coast. Recent flooding has reinforced that properties outside commonly recognized high-risk areas can still experience significant flood damage.

Therefore, buyers should investigate a property’s flood risk rather than assume that “not in a required flood zone” means “no flood risk.”

FEMA Flood Map Service Center | Search By Address

Homeowners insurance has become an increasingly important part of the total cost of owning a home in Texas.

Are Texas Homeowners Insurance Rates Finally Stabilizing?

There is some reason for cautious optimism.

After average statewide rate increases of 21.1% in 2023 and 18.7% in 2024, the average increase slowed to 4.3% in 2025. Recent reporting also indicates that Texas home insurers had a significantly stronger financial year in 2025.

However, I would not interpret that as a promise that premiums are about to fall.

Texas remains exposed to severe weather. Rebuilding costs remain important. Additionally, insurance pricing varies significantly by location and property.

The better way to describe the current situation is this:

Texas homeowners insurance remains dramatically more expensive than it was five years ago, but the pace of statewide rate increases slowed considerably in 2025.

For homeowners and buyers, that’s better news than another year of double-digit increases. Still, affordability remains a real concern.

What I Tell Central Texas Homebuyers

My advice is simple: don’t treat insurance as an afterthought.

Before becoming emotionally committed to a property, understand the major costs associated with owning it.

A home can look affordable based on the purchase price and mortgage payment. However, higher property taxes and insurance can change the numbers quickly.

On the other hand, a home with a newer roof, favorable insurance characteristics, and lower ongoing expenses may be a better long-term value—even if its purchase price is slightly higher.

That’s why I believe buyers need to look at the whole financial picture, not just the asking price.

Frequently Asked Questions About Texas Homeowners Insurance Rates

How much have Texas homeowners insurance costs increased?

Recent reporting based on Texas insurance data indicates that the average Texas homeowners policy cost roughly 80% more in 2025 than in 2020. However, individual premiums vary significantly by property and policy.

Did Texas homeowners insurance rates go down in 2025?

Not on average. However, the pace of increases slowed considerably. The average statewide rate increase was reported at 4.30% in 2025, compared with much larger increases in 2023 and 2024.

Does a $400,000 home have a standard insurance cost?

No. The home’s purchase price alone cannot determine its insurance premium. Location, replacement cost, roof condition, coverage, deductibles, claims history, and other factors can affect the cost.

Should I get an insurance quote before making an offer?

At minimum, buyers should begin thinking about insurability early. Once you’re seriously considering a specific property, getting a property-specific quote as soon as practical can help you understand the total monthly cost.

Does homeowners insurance cover flooding?

Standard homeowners policies generally do not cover flood damage. Flood insurance is typically separate, so buyers should investigate both flood risk and available coverage.

Final Thoughts on Texas Homeowners Insurance Rates

The last five years have changed the cost of homeownership in Texas.

Mortgage rates get most of the headlines. Property taxes generate plenty of discussion. However, homeowners insurance has become an increasingly important part of the affordability equation.

The encouraging news is that the pace of Texas rate increases slowed substantially in 2025. Nevertheless, today’s premiums remain far higher than they were five years ago.

If you’re planning to buy a home in San Marcos or anywhere in Central Texas, I can help you look beyond the list price and evaluate the bigger picture.

That includes the property, the market, estimated taxes, insurance considerations, and the other factors that can affect your monthly cost of ownership.

Central Texas Home: Is Now a Good Time to Buy in 2026? – Walker Texas Team

Search Central Texas Homes for Sale → Search Listings – Walker Texas Team

Thinking about buying or selling in Central Texas? Contact James Walker and the Walker Texas Team at Keller Williams Realty to discuss your real estate goals and the true costs involved in today’s market.

James Walker

Associated Broker

Team Lead, Walker Texas Team

Keller Williams Realty

Walker Texas Team at Keller Williams Realty KW ATX—trusted real estate experts serving San Marcos, TX and the Central Texas area.